My conversations with Leonard Lee, Dr Michael Kollo and Adam Acar while recording the Wealthy Tiger podcast series has prompted me to revisit some old ideas about network effects

Specifically the impact of share of voice has on accelerating network effects and to what extent share of voice can help us forecast crypto adoption

We'll begin by exploring this idea of share of voice

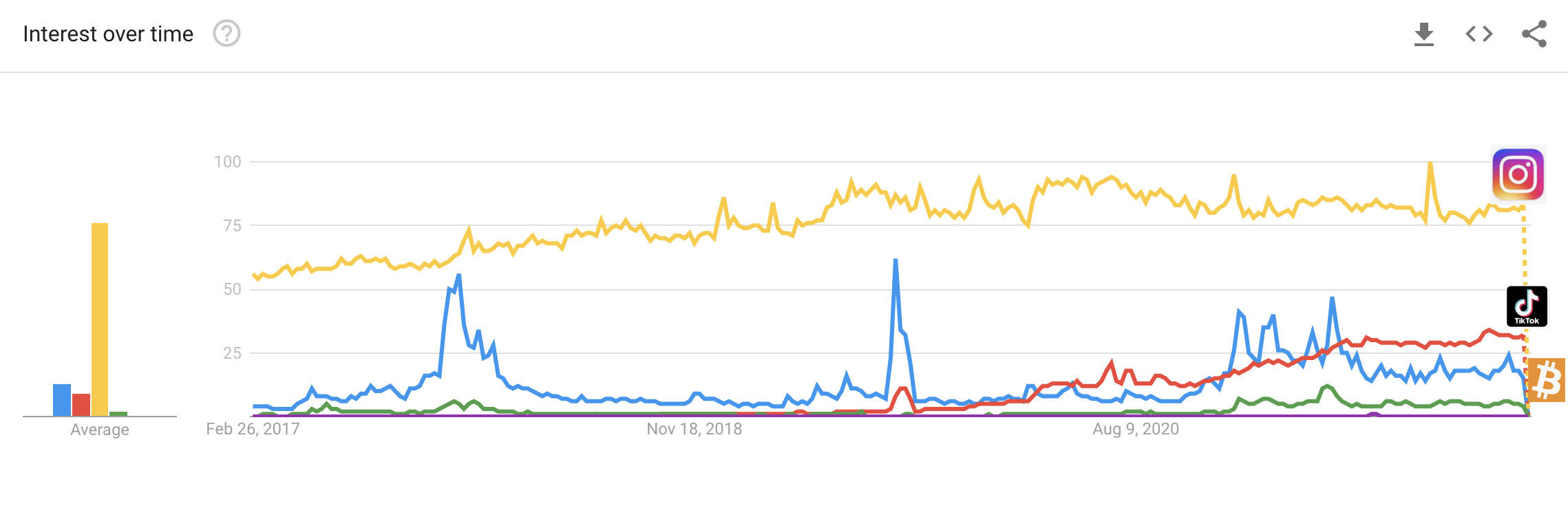

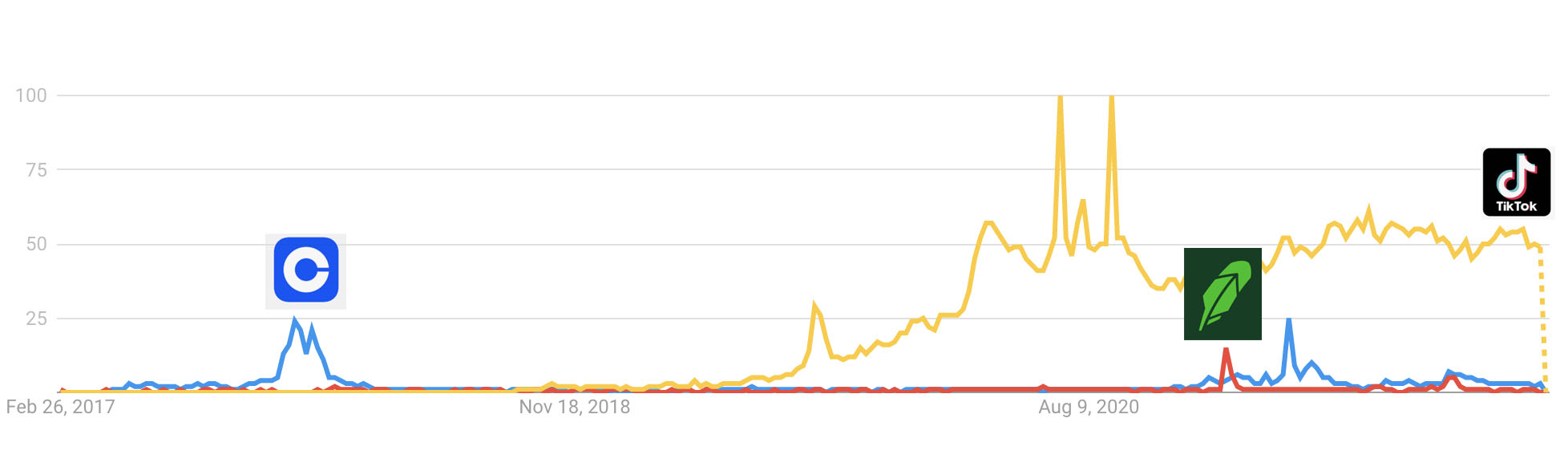

Here is the Google Trends data comparing - among many things - Facebook, Instagram, TikTok and Bitcoin

As you can see Facebook has dominated share of voice for most of the past 2 decades

Love it or hate it. Be in no doubt. We love to talk about it

and for all the hype Crypto - in all it's forms - doesn't come close to dominating share of voice

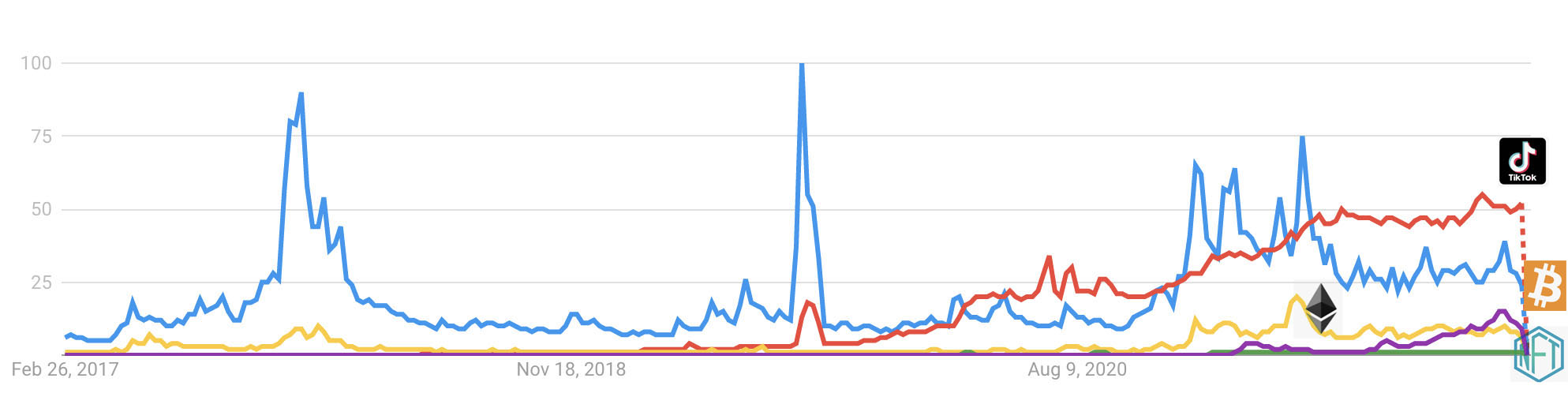

So let's strip Facebook out of the equation

We now see Instagram dominates share of voice

Strip Instagram out of the equation and we discover, Bitcoin - powered by the crypto bubbles - is competing with TikTok as the emergent network effects story of the past 5 years

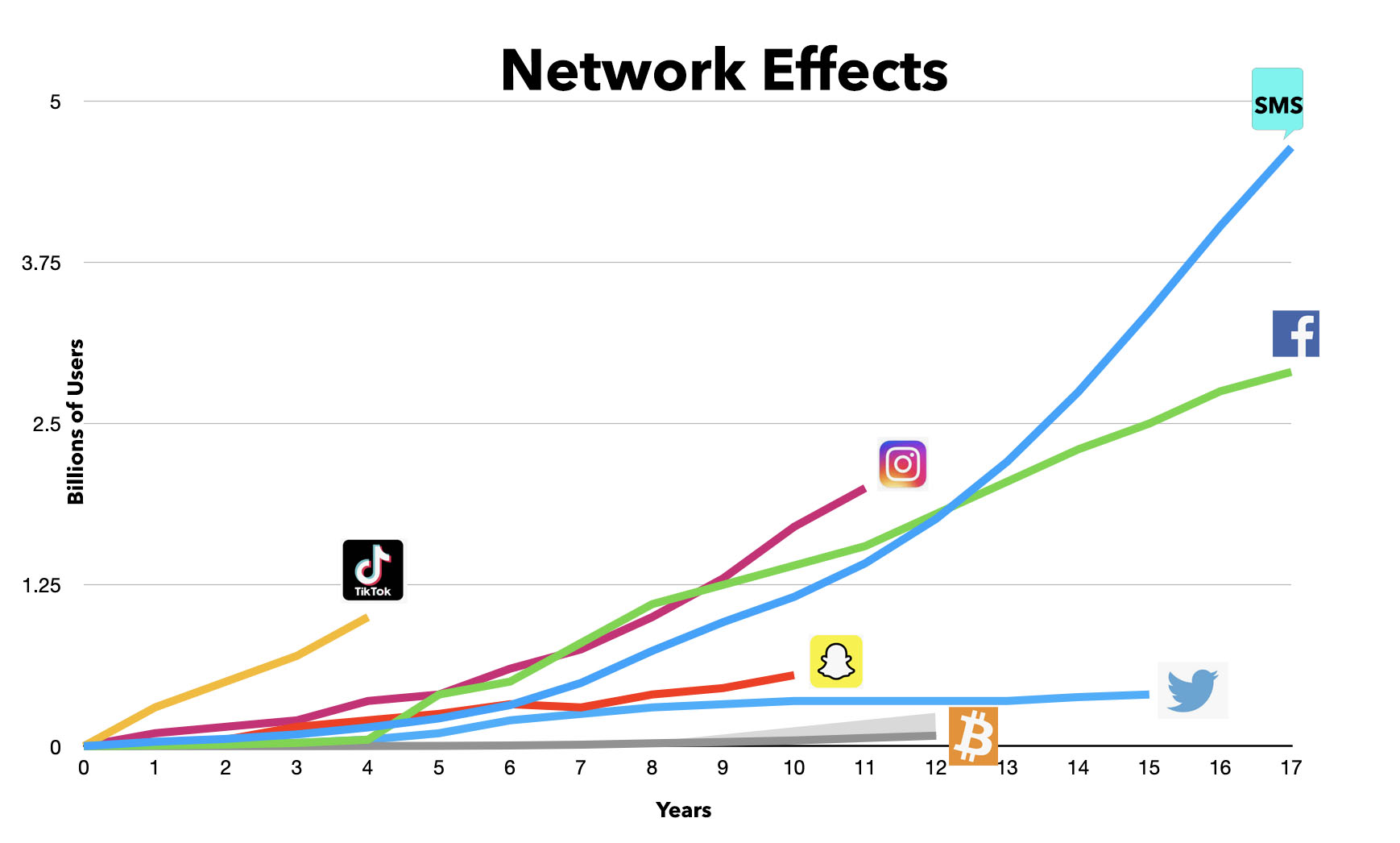

Now let's take a look at how that share of voice translates into network effects

We discover two things. When it comes to measuring network effects SMS is still the benchmark but TikTok is on track to be the new Benchmark if it can sustain its growth trajectory

and what about crypto?

Well we can see clearly, despite all the hype and all the money spent on PR by Venture Capitalists and early investors promoting Crypto as the next wave of disruption to capitalise on the power of network effects, it isn't... capitalising on the power of network effects

By any measure of the mathematics of network effects crypto adoption is slow by web standards

and, apparently slowing down compared to the early internet, at least prior to the 2021 crypto bubble

But is it?

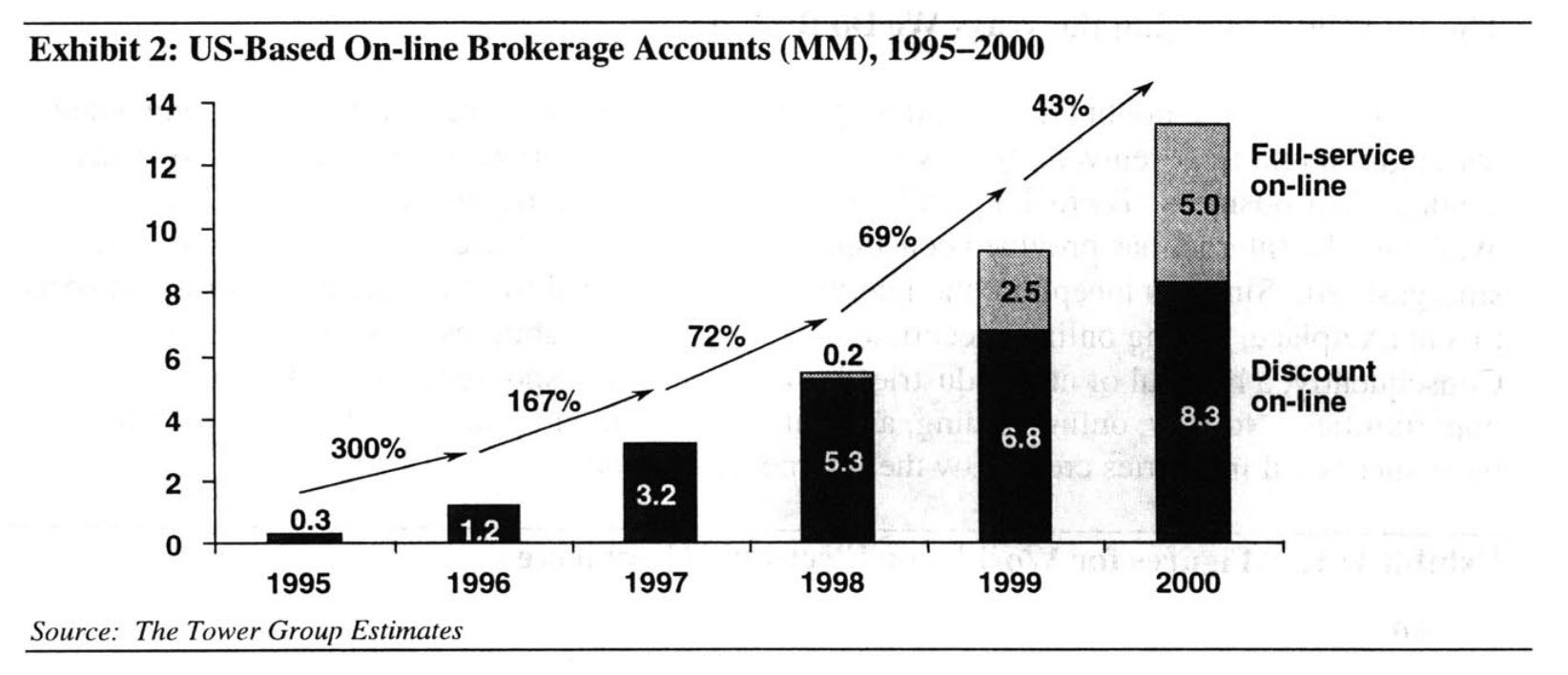

Roll back the time clock to the early days of the web and we discover - once we adjust the numbers for the realtive scale of the web between 1995-2005 - we discover crypto user numbers track the online trading numbers

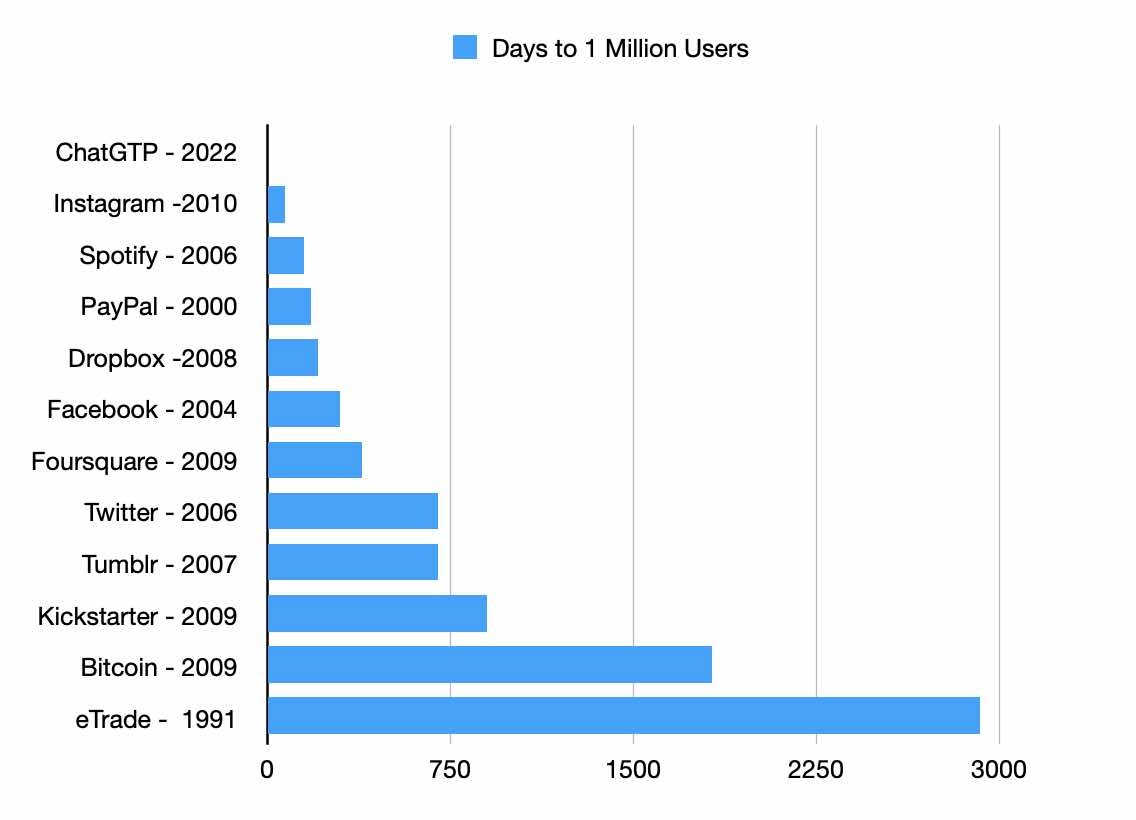

Source MIT - Online Trading: An Internet Revolution

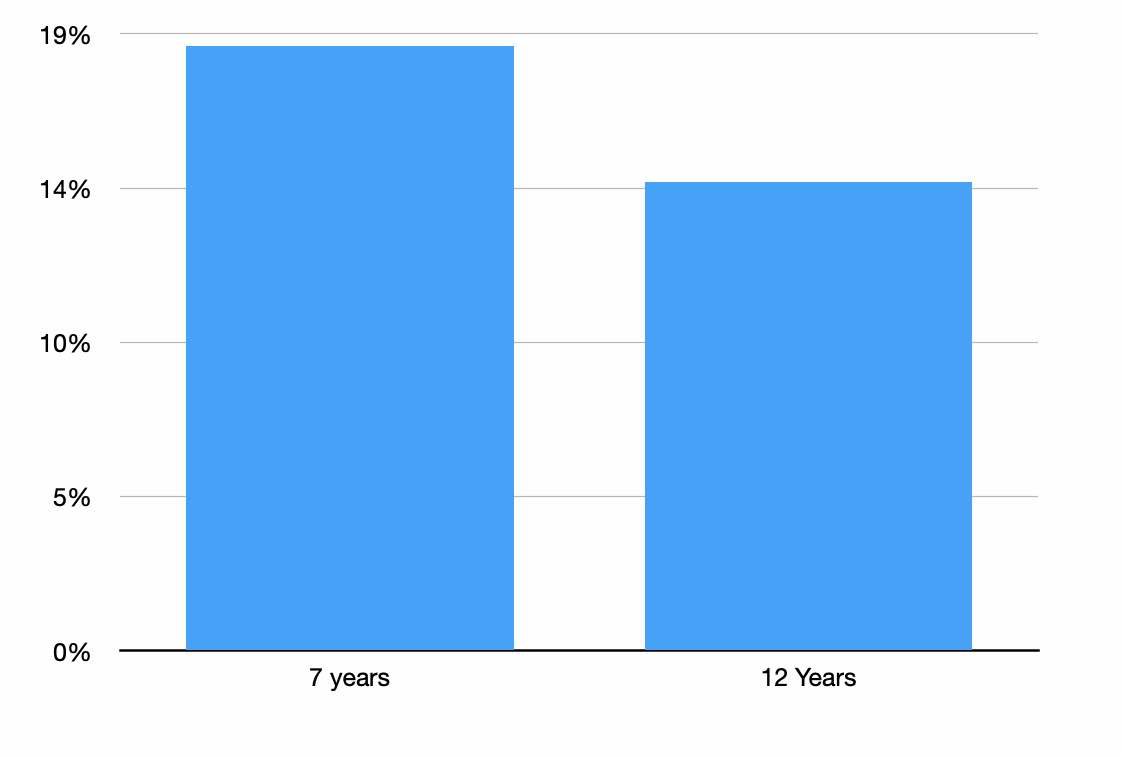

In 2000 (about 10 years after the first online broker opened their doors) 9% of US Internet users had an online trading account

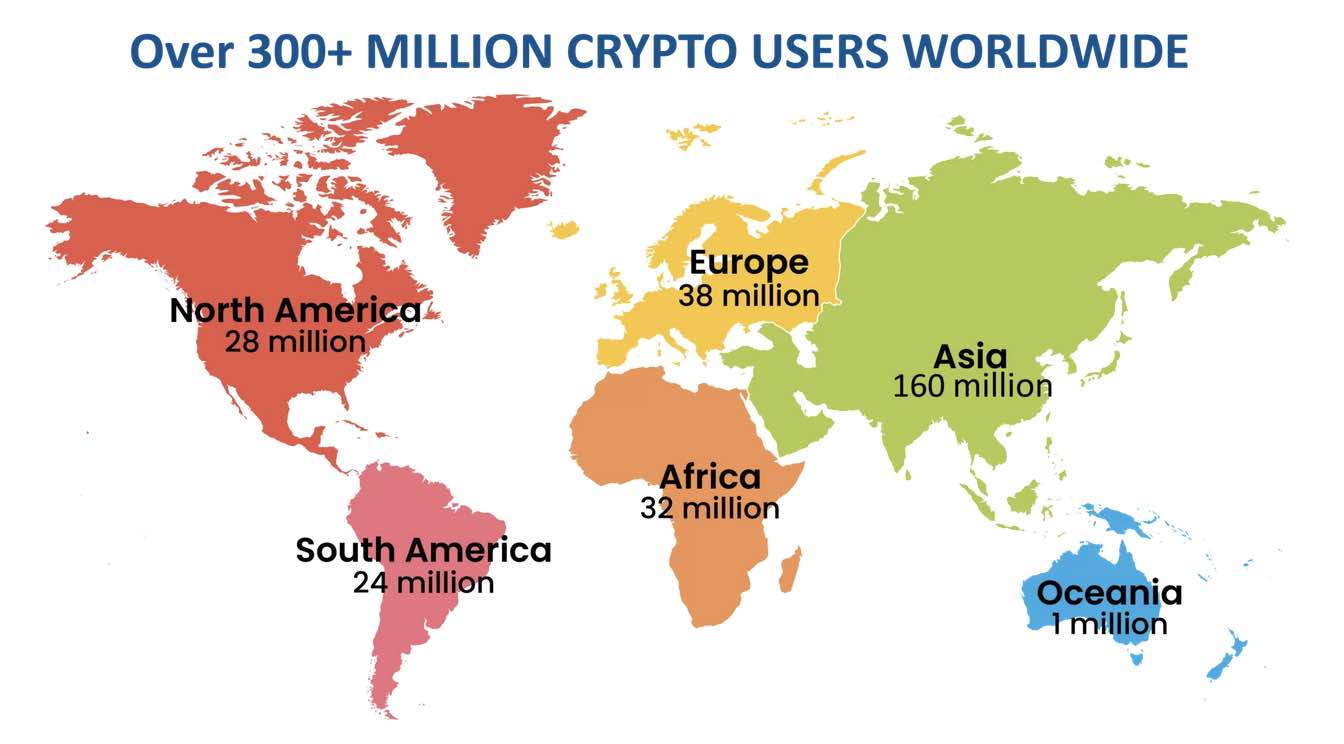

13 years after the first Bitcoin was mined we discover about 8% of US & Canadian Internet users are crypto users

Now arguably crypto adoption lags Web 1.0 online trading adoption but, more importantly, this also suggests crypto is a niche product.

It appears to be attracting the same market that was attracted to online trading (Some would argue this is self evident)

and... 30 years on we discover that less than 20% of US internet users have online trading accounts

This discovery also suggests the size of the crypto market should be relatively easy to estimate

An assumption that is supported by the share of voice for trading apps vs TikTok

Now… where does that leave us in the grand scheme of things?

Well today there is an assumption Crypto is early in the adoption cycle

However the online trading adoption data suggests this may be false

If we remap crypto adoption curve to the 30 year online trading adoption curve we discover the potential market for crypto may have already achieved 50% adoption within its Serviceable Available Market in key markets like North America

Now dare I say that's something to think about...

At least until next time :)

Postscript:

In retrospect - despite all the media hype - this weak adoption trend was apparent within the first 12-18 months of the launch of Bitcoin

Which is to say by 2012 it was self evident Bitcoin was no PayPal 2.0 (ie it didn't solve a pressing problem in the world of digital commerce)

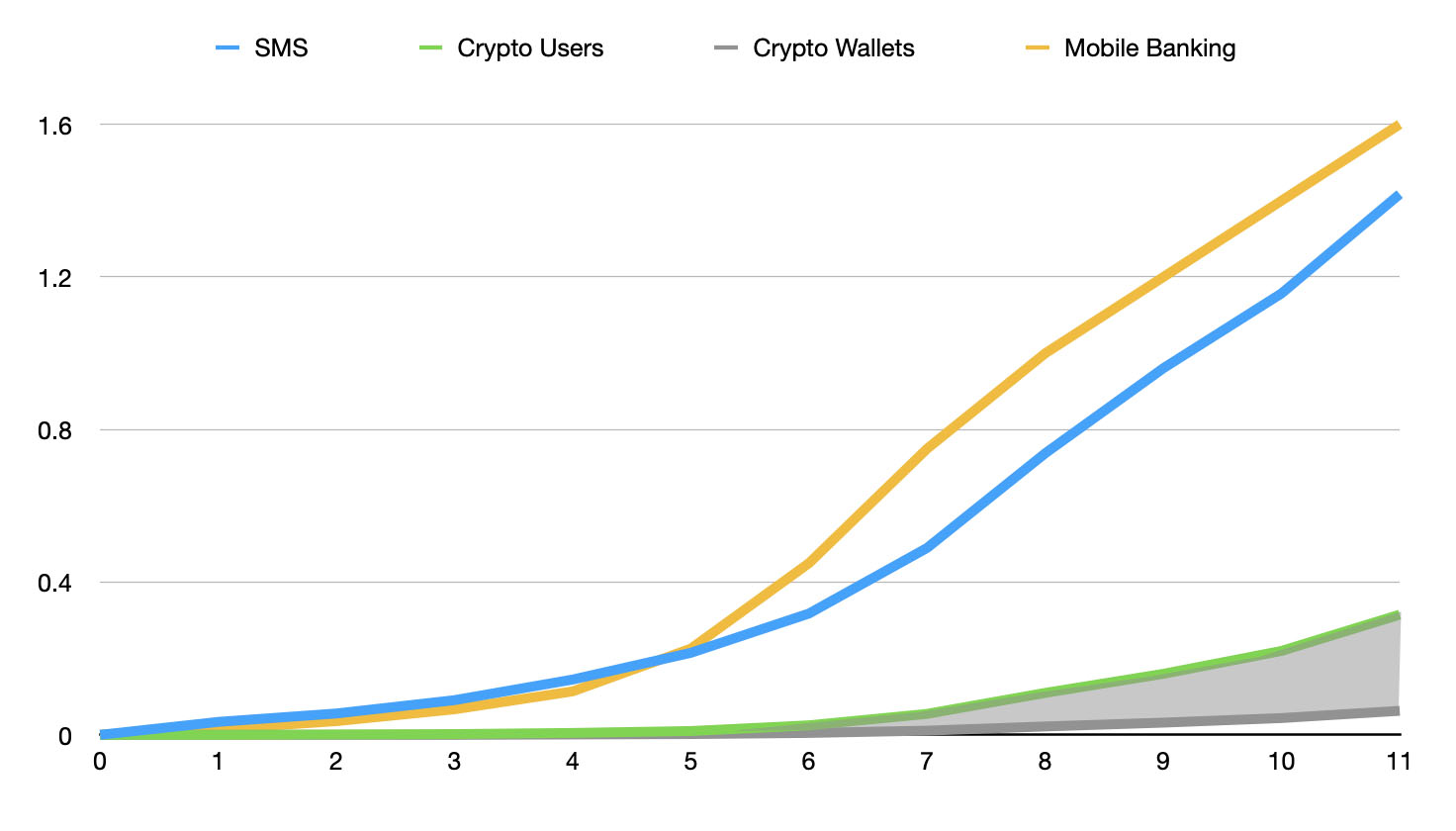

and this raises the question: How does Crypto compare to user adoption of mobile banking?

Well in the USA it took 13 years for user adoption of mobile banking to hit 50%

Meanwhile the adoption rate in China has been even faster

Today there is an estimated 1.9 Billion mobile banking users world wide

i.e over 6x the estimated number of crypto users

Suggesting the network effects of mobile banking look a lot like SMS and Facebook