Originally Published Autumn 2021.

A few days ago Fred Wilson from Union Square Ventures, one of the brightest stars of this generation of VCs, posted a summary of their portfolio returns

Needless to say it has proven popular in VC circles as an illustrative proof of the efficiency of investing in Venture Capital

After you scan the list you will note that he chose not to compare these results with investing in the passive market index... having assumed, naturally enough, that all but a few of the portfolio vintages beat investing in the market index

So, as a quick thought experiment, I thought I'd put this assumption to the test

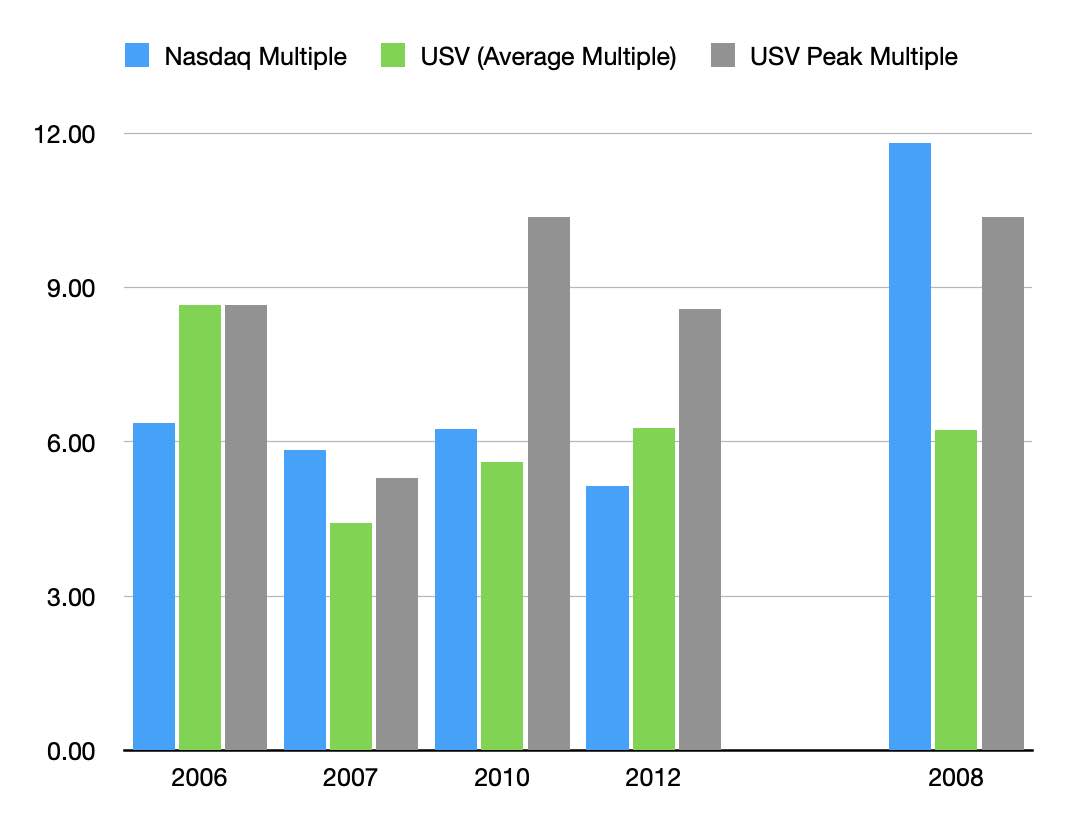

Scanning the list we discover the medium multiple of the vintages is 4.7x

This looks like a great ROI... but what about investing in the NASDAQ 100 during those vintage years?

Well we discover the median multiple scattered across those vintage years is 6.8x

We also discover that only about a 1/3rd of the portfolio vintages actually beat investing in the passive market index.... and none of the vintages beat investing in the index in late 2008

and I think there is a lesson in there - about how narrative shapes our ideas about innovation

At least for those who are prepared to going looking

Because, if you take the time to look are little closer at the Venture Capital industry, you discover Union Square's performance isn't the exception... it's the rule

Moreover, the industry's ability to misread the data appears to be almost universal

For example Michael Jackson posted a link to a post by Dan Malven (See Here )

Dan's post is a commentary on a NBER study VC of returns (See Here )

One of the key observations is

"The authors debunk the old chestnut that there is 'too much money out there chasing too few deals' by showing that VC industry capitalization remains at relatively low to medium historical levels of 0.10 to 0.15 percent of total stock market capitalization. When VC industry capitalization is at low to medium levels, the next five to 10 years of VC industry returns are expected to be strong.”

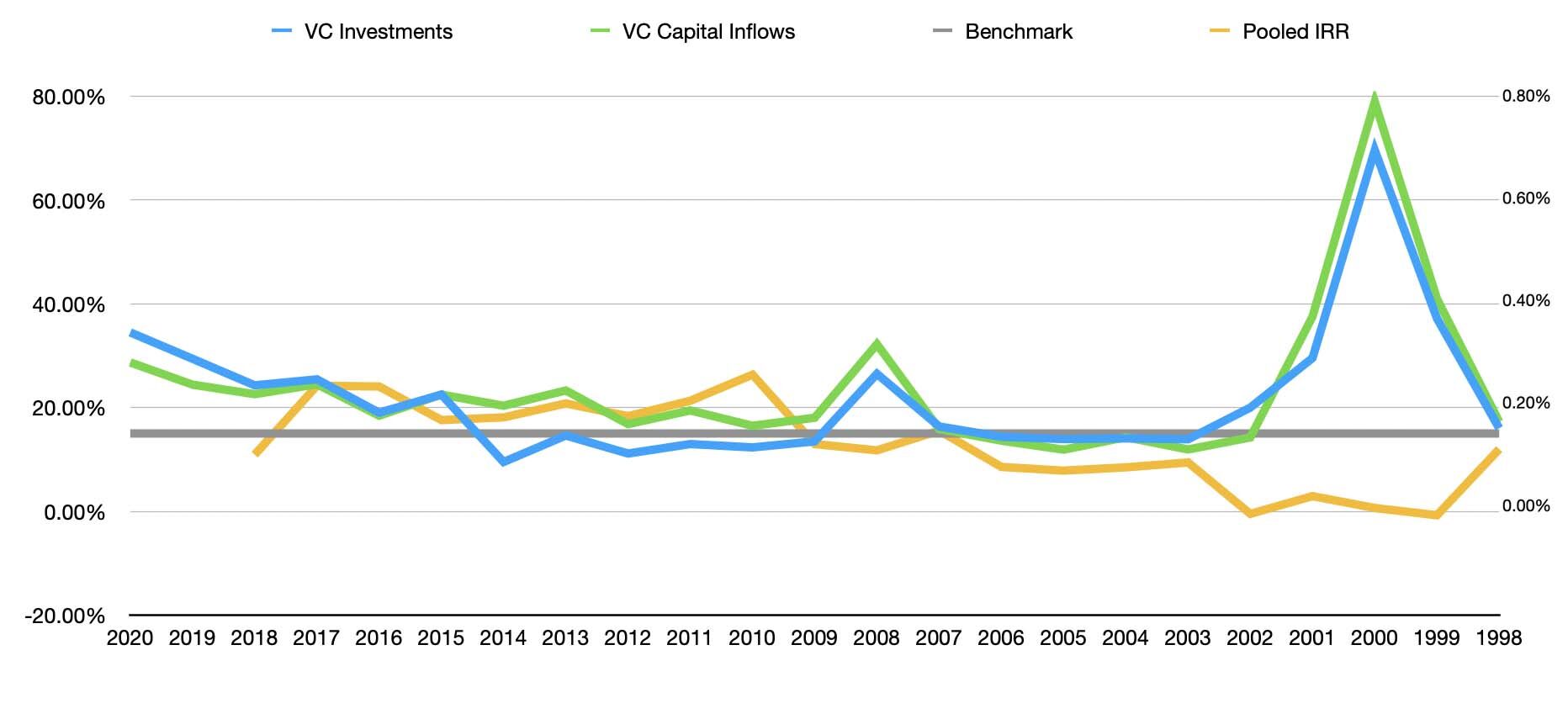

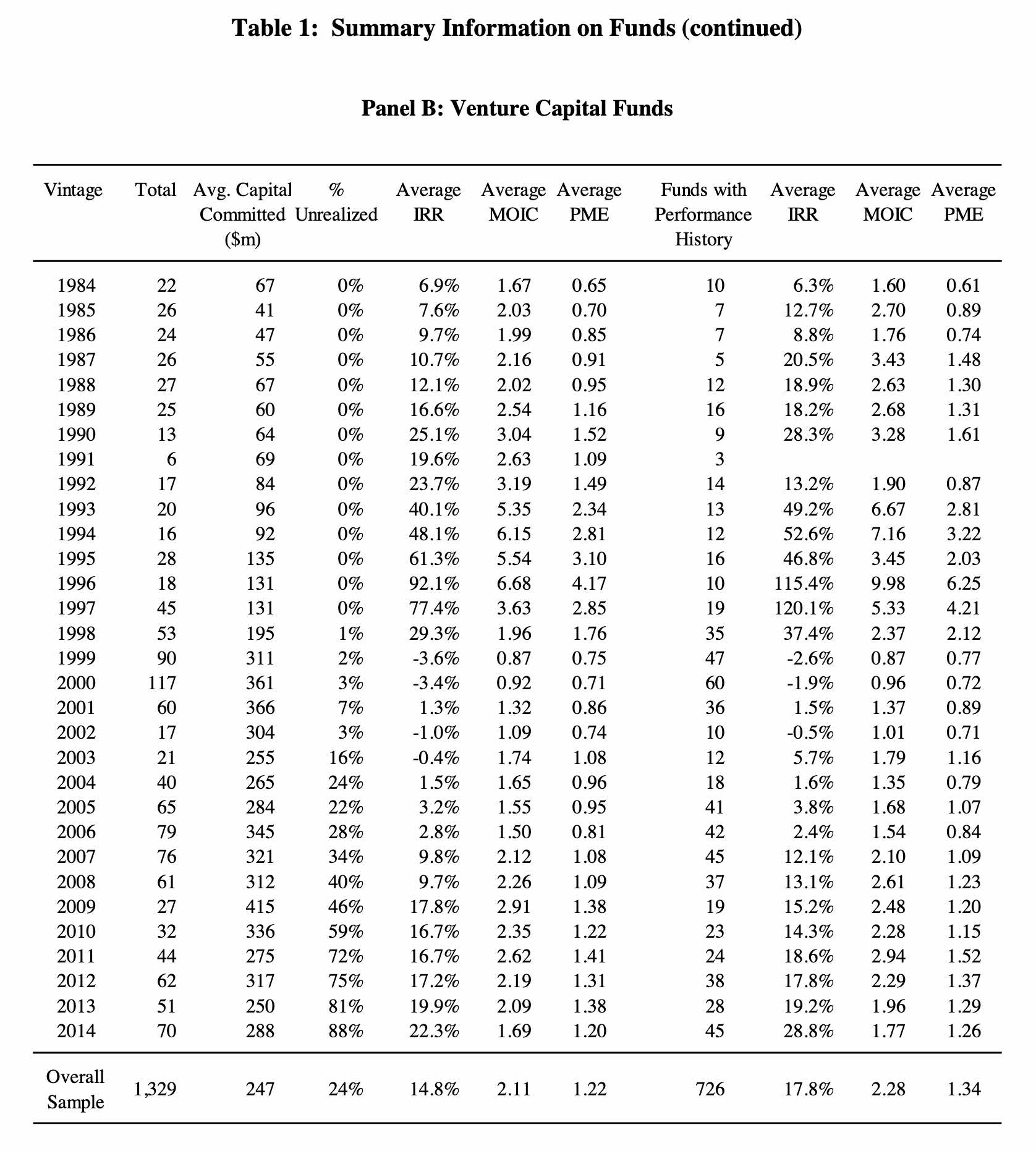

I thought I'd put it to the test by harvesting a few numbers

As you can see the post GFC VC performance does not correlate with the post-Dot Com Boom period suggesting this proposed rule of thumb is open to question.

Moreover the current ratio of VC industry capitalization is much higher than the proposed rule of thumb

Suggesting perhaps, rather than debunking the old chestnut, the industry data tends to confirm it...

Dig a little deeper into the the data published in the research paper Dan is commenting on and you'll discover the case for Venture Capital made by the authors is a forecast. A projection.

But that doesn't stop the VC's publishing these statistical estimates as evidence of Venture Capital's ability to outperform passive investing

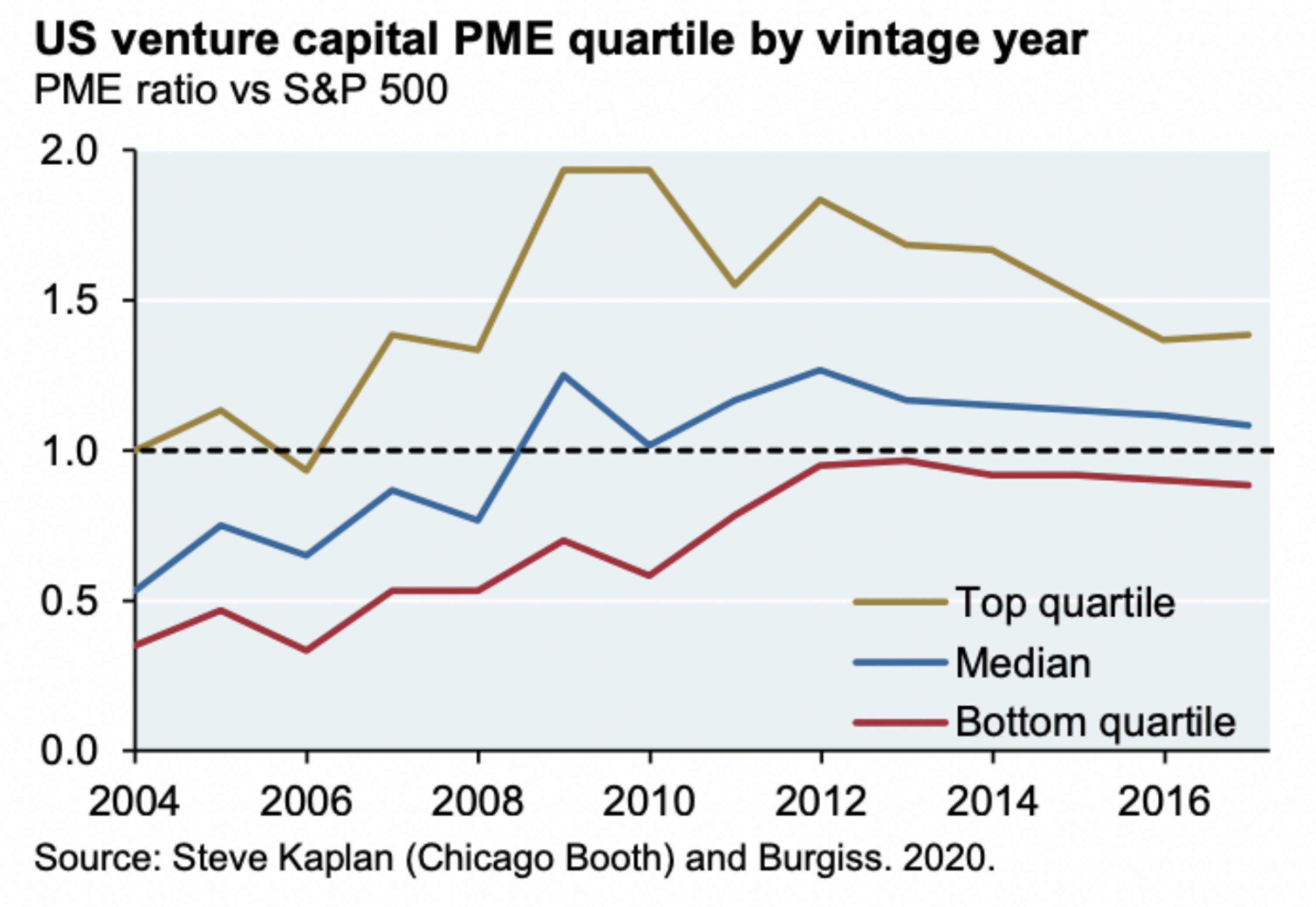

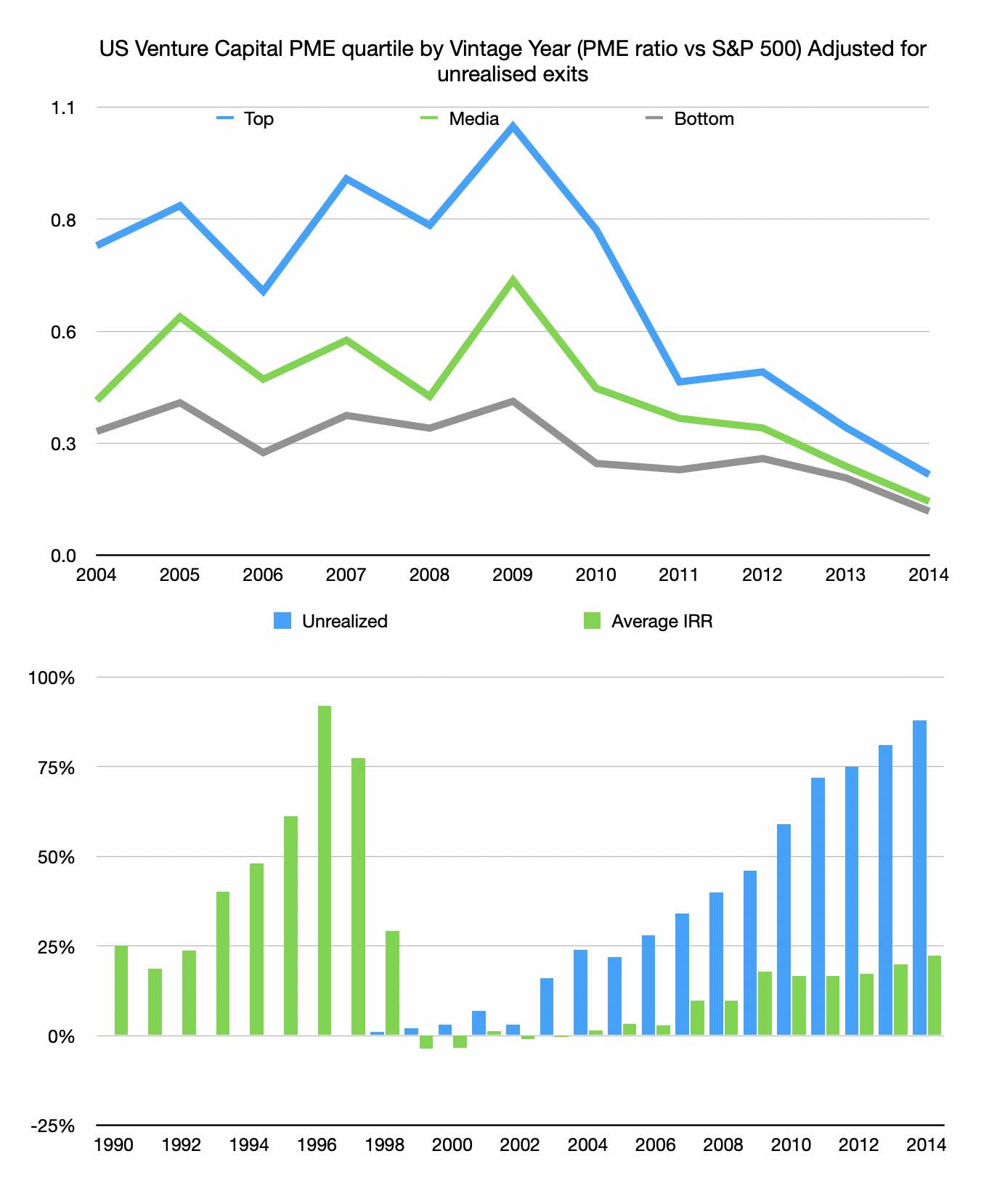

Adjust these figure to take into account the unrealised exits of the FUM and we discover a very different story

Here is the data sample that we have used to normalise the projection

This is what the average IRR looks like adjusted for unrealised gains

As you can see 20 years on the post Dot-Com performance does not match the decade that delivered the Dot Com Boom

It appears even during the longest Tech Bull Run in history and the US Federal Reserve pumping in trillions of $$$$$$$ into the markets the industry has a problem with exits

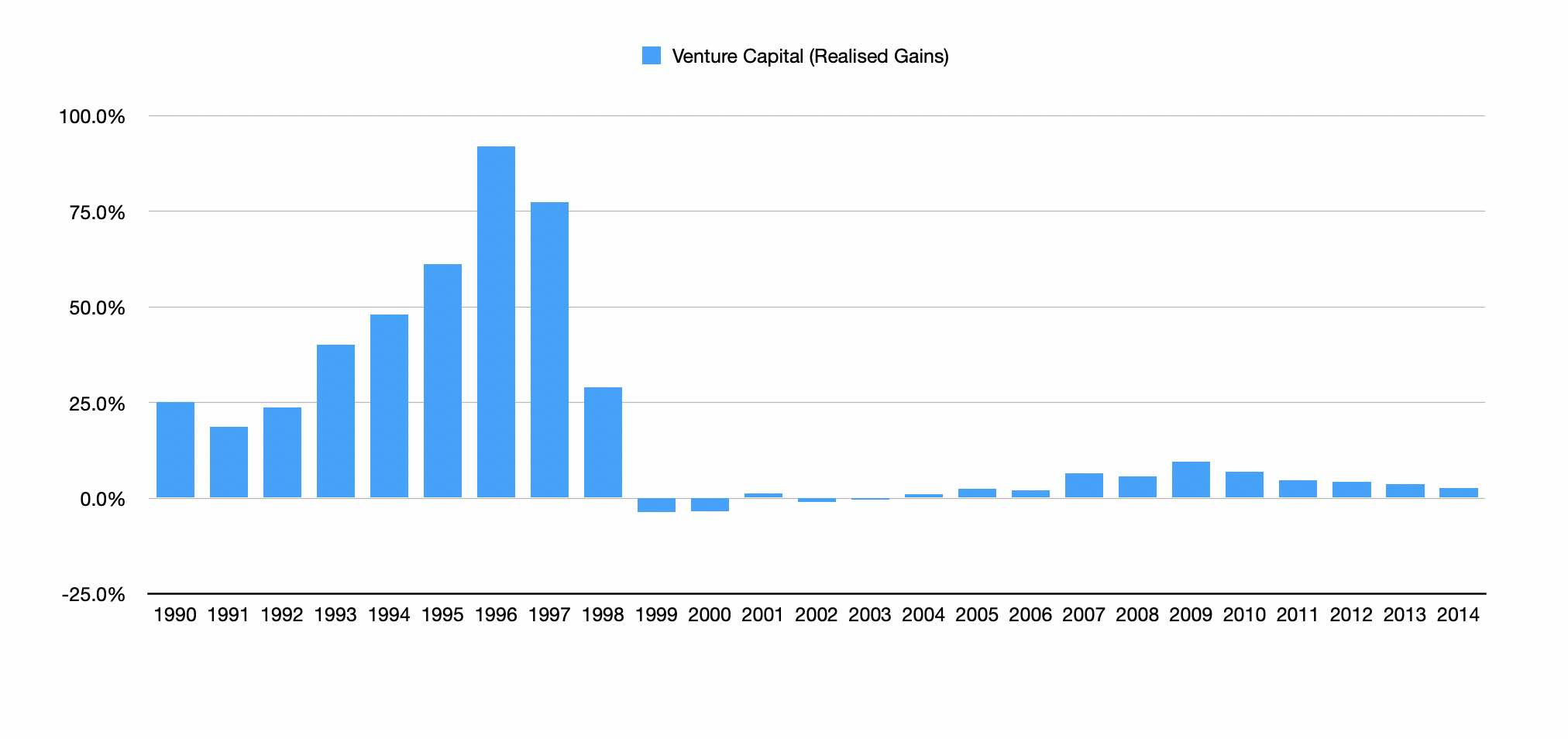

Now let's map those returns against passive investing over the same period

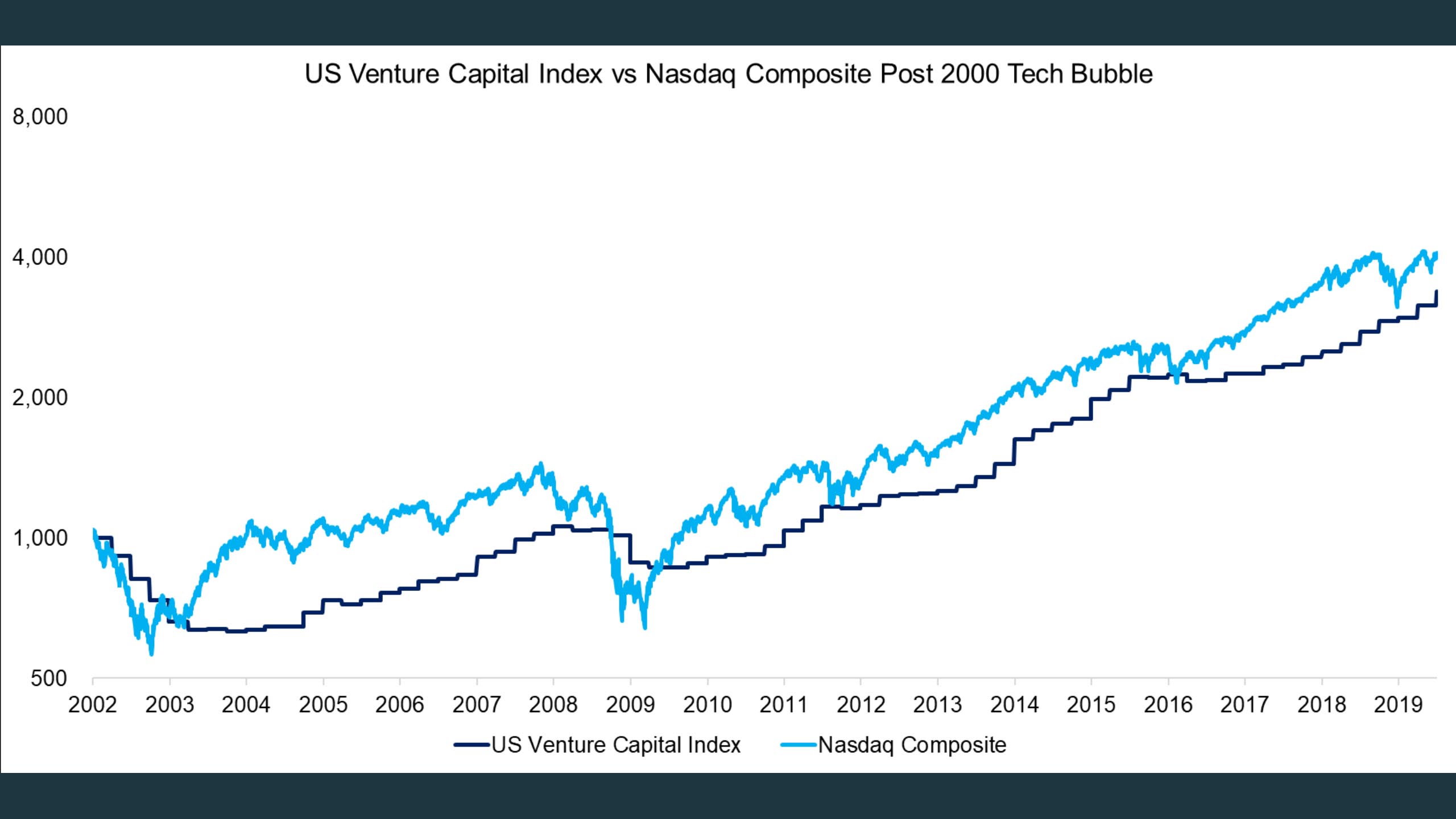

... and yes we discover what has been widely reported over the past 20 years

Since the Dot Com bust venture capital has struggled to replicate the outsized returns of the 1990's

Moreover, like much of the active money management industry, it has stuggled to compete with passive investing

This struggle reflecting the broader market reality: ie. The pace of technology adoption has slowed, rather than accelerated, since the turn of the century

Update Autumn 2022

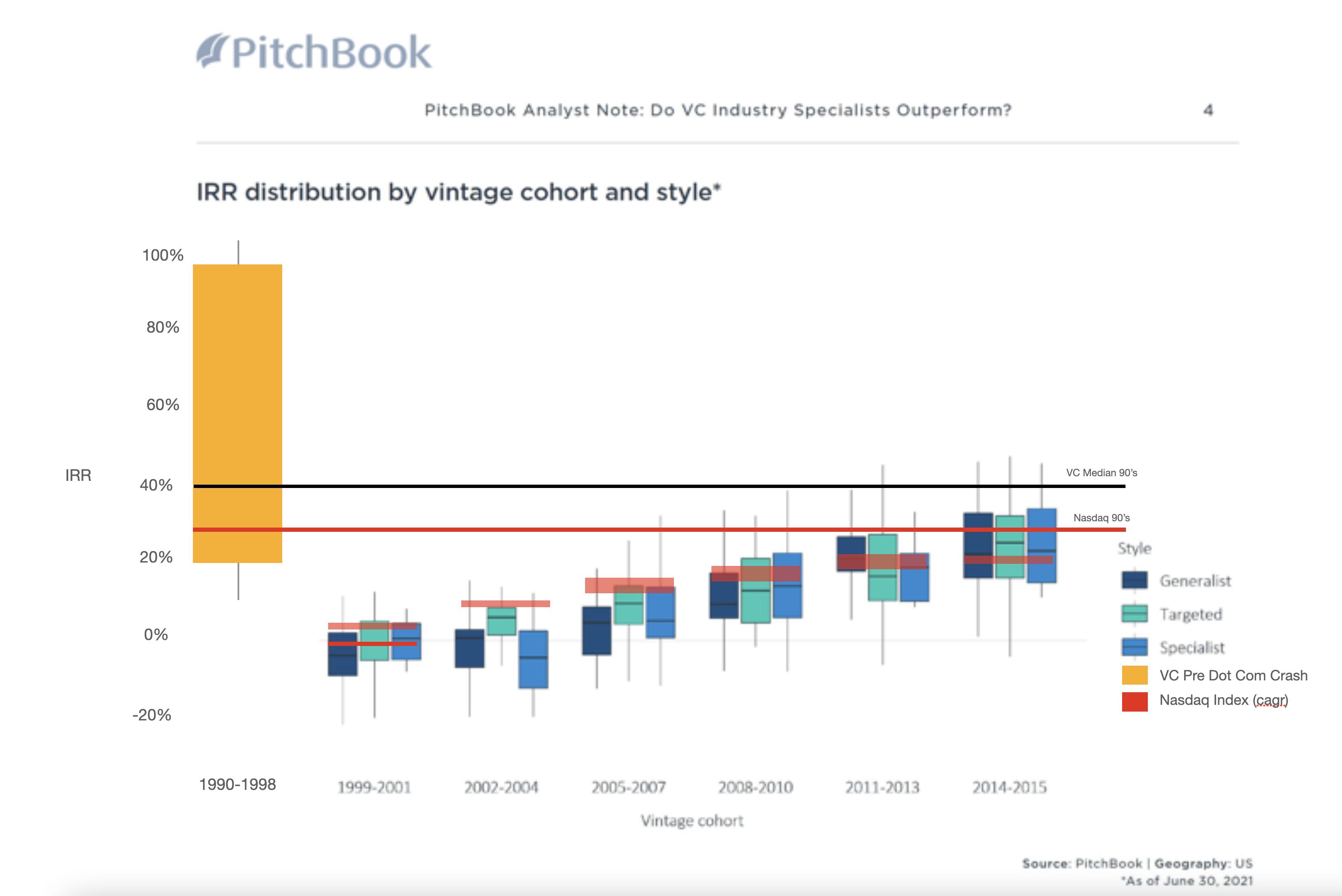

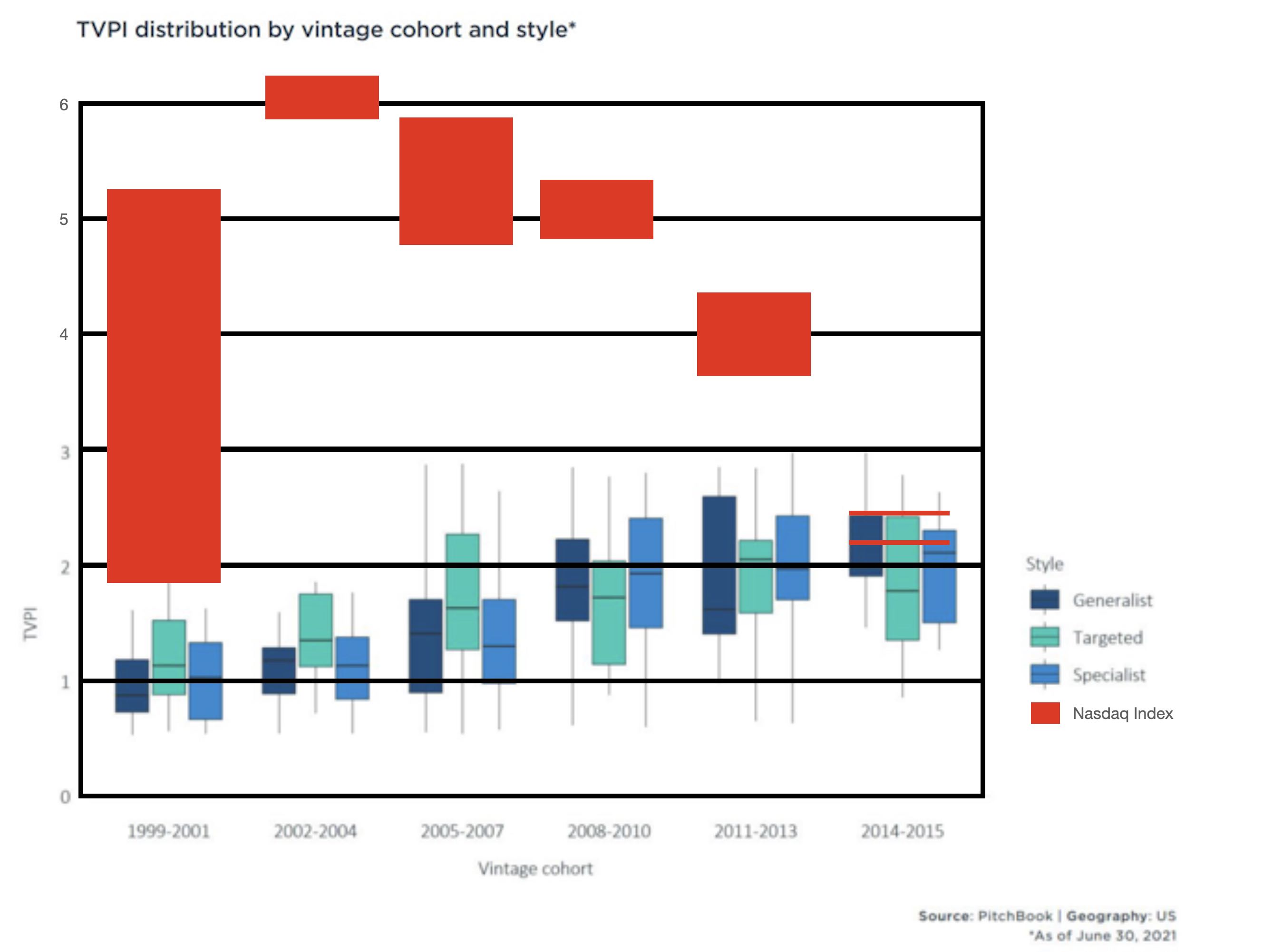

One year on from this initial investigation Pitchbook released a data set from June 2021 comparing the relative performance of VC investment styles.

So let's take this opportunity to update the original analysis with the new data

We'll begin with the relative performance of 21st Century VC IRR vs the historical performance of both the industry and the Nasdaq

The basic observations are

a. The pandemic/crypto bubble has improved the relative performance of portfolio managers against the passive index in recent years

b. (But) Even with the bubble 21st Century VC performance is still below the median performance of the industry during the 1990's and well off the peak returns of the mid-1990's

Moreover - once you switch to TVPI = we discover the relative performance against a simple buy and hold passive investing strategy the industry's performance continues to be relatively weak by historical measures

Further proof - if any more is needed - that venture capital continues to be an industry that lives off the memory of its past reputation for delivering outsized returns in exchange for investors taking outsized risks on illiquid assets

Update Autumn 2023

Two years on and Pitchbook have released a list of the top performing VC funds since the dotcom era

So let's take this opportunity to once update the original analysis with the new data

As you can see the passive investor who could time investing at the GFC low and exiting at the peak of the 'everything bubble' delivered a return that placed them easily within the Top 5 of 1500+ VC funds

and even if you had no appetite for timing the market and merely invested at the beginning of 2010 and held until today (May 2023) you are within the performance capability of a Top 30 VC fund manager

and this of course raises the question why?

Why do VCs struggle to outperform passive investing?

Well perhaps the simple answer is they have an exceptional talent for picking losers... because, when you think about it, all that talk about investing outliers - those founders who can hit the ball out of the park - is really just another way of saying we take a heck of a lot of swings (and misses) on the off chance we might get very lucky