Last year Accenture invited us to spend autumn in Hong Kong with the innovation teams at BNP Paribas, Bank of America Merrill Lynch, Commonwealth Bank of Australia, Credit Suisse, Goldman Sachs, HSBC, J.P. Morgan, Macquarie Group, Morgan Stanley, Nomura and Sun Life Financial. The focus was on defining the market fit of our "distributed ledger of probabilities" forecasting technology within the Financial Services & Insurance Sectors.

We decided to utilise our time there to build a Robo-VC model.

Our thinking was: It is seven years since Marc Andreessen proclaimed in the WSJ: "Software is eating the world".

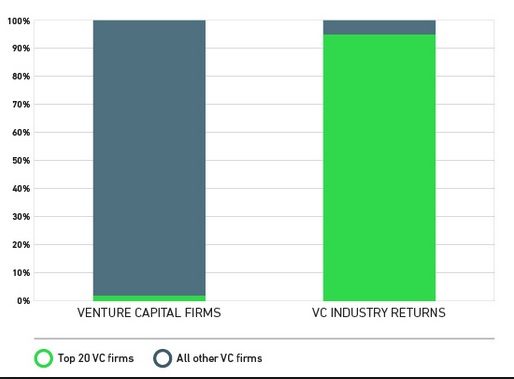

Today Venture Capital is a $0.5 Trillion Global 'Cottage Industry'. Raking in over $10 Billion in administration fees

...and yet less than 5% of VC's utilise in-house data analytics at scale.

So we decided to investigate the question: Can software eat venture capital?

Just how hard would it be to build an Artificial Intelligent Venture Capitalist (Think: RoboVC) that could not only compete with the market... but beat the market?

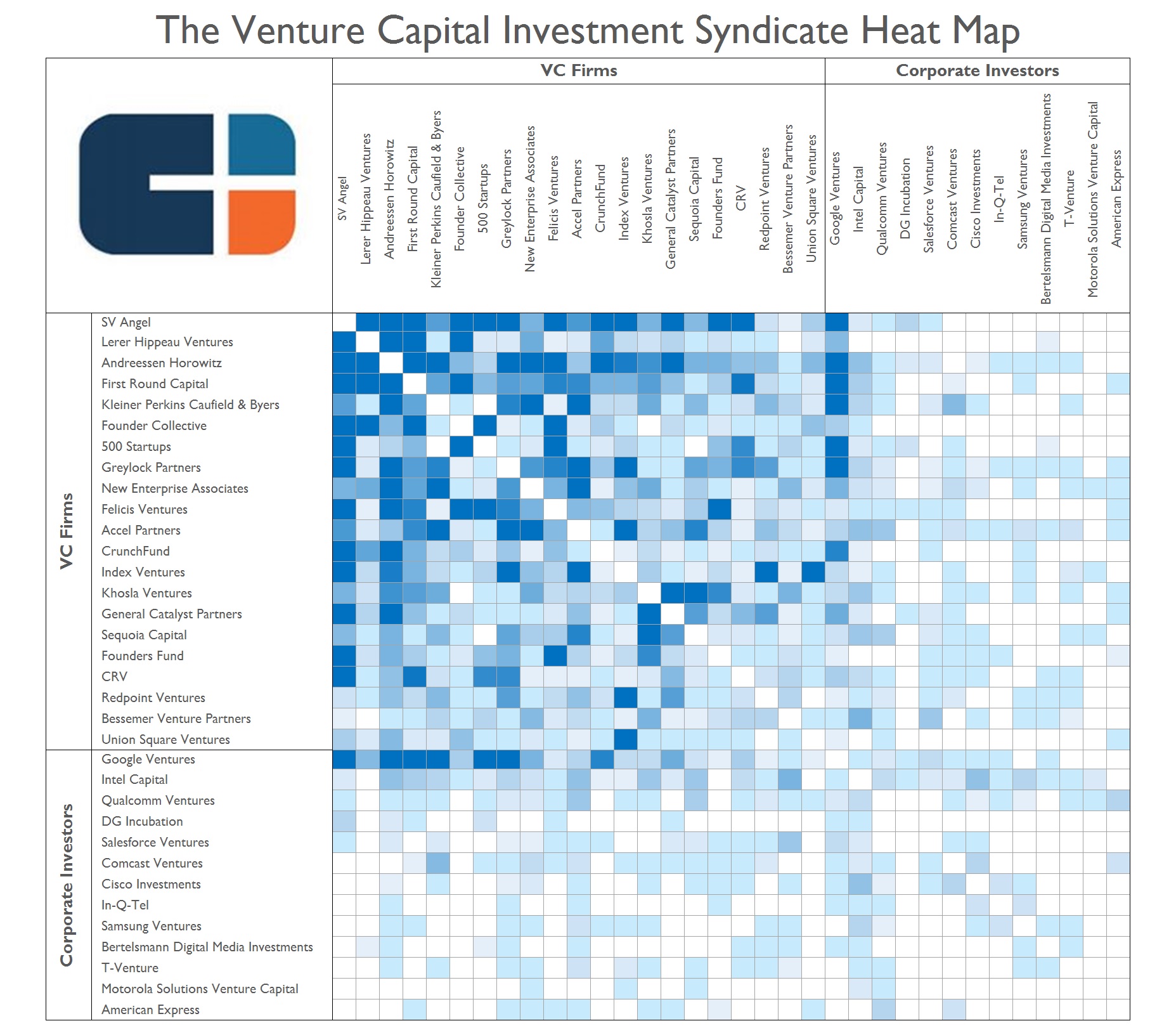

We began the journey by looking for patterns of divergence, convergence, emergence and contagion in the publicised industry data

What we discovered surprised us.

The familar, widely endorsed patterns of investment behaviour at the group portfolio level...

Didn't hold up at the individual investor level.

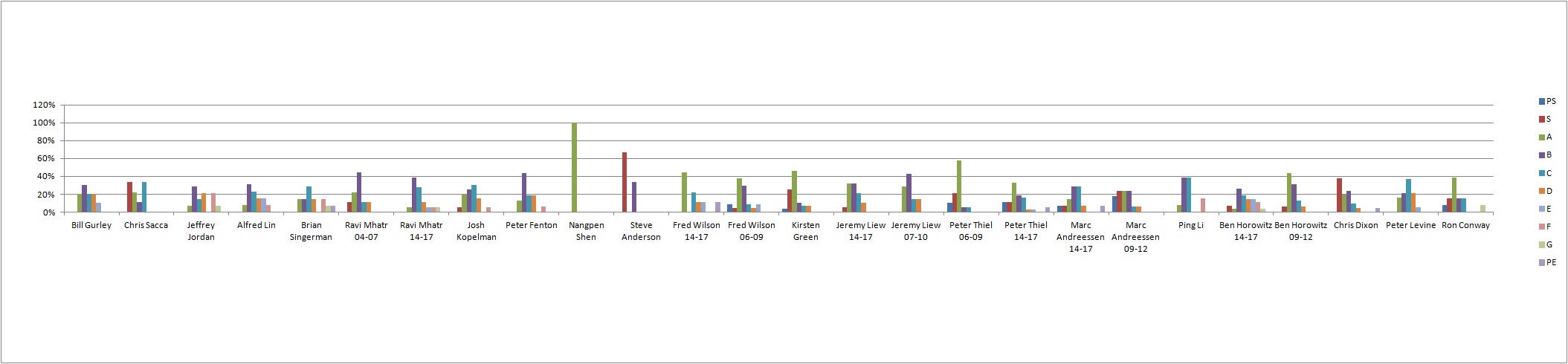

Mapping the habits of the Top 100 VC's revealed a random walk.

What sports enthusiasts would call a case of "Hot Hands".

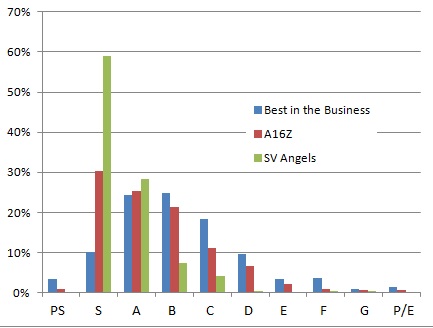

Suggesting the popular insights published by the leading VC's on how to profit from the great disruption of paper to be nothing more than stories of survivour bias.

This meant our journey was not just about automating industry best practice but one of deconstructing the narrative to discover the exceptions that prove the rule.

The signal in all the noise.

To demonstrate that venture capital portfolio management correlates with a random walk here is a market simulation comparing VC Investment Strategies with gambling at the Roulette Table.

This first chart maps the random walk of 10 VCs placing 10 Bets per Year for 10 Years at the Roulette Table.

The model demonstrates the random returns of the baseline bet for each VC Portfolio plus the impact of 'Doubling' down and/or 'Spread Betting' on subsequent bets if they win.

If you re-run the simulation 10x you will see a pattern of 'Hot Hands" emerging from the random walk.

It is evident that Investment Returns in excess of 4x can be achieved simply by being:

a. Lucky, and

b. Playing the right "investment" Strategy