Originally Published Spring 2018.

Last year Accenture invited us to spend autumn in Hong Kong with the innovation teams at BNP Paribas, Bank of America Merrill Lynch, Commonwealth Bank of Australia, Credit Suisse, Goldman Sachs, HSBC, J.P. Morgan, Macquarie Group, Morgan Stanley, Nomura and Sun Life Financial. The focus was on defining the market fit of our "distributed ledger of probabilities" forecasting technology within the Financial Services & Insurance Sectors.

We decided to utilise our time there to build a Robo-VC model.

In our first post we demonstrated how VC investment is a random walk.

This model explores the idea that Venture Capital portfolio optimisation is a function of the market... Or, more accurately, the portfolio manager's relationship with the market. Rather than the individual portfolio manager's ability to consistantly pick winners.

The rules behind this model are very simple.

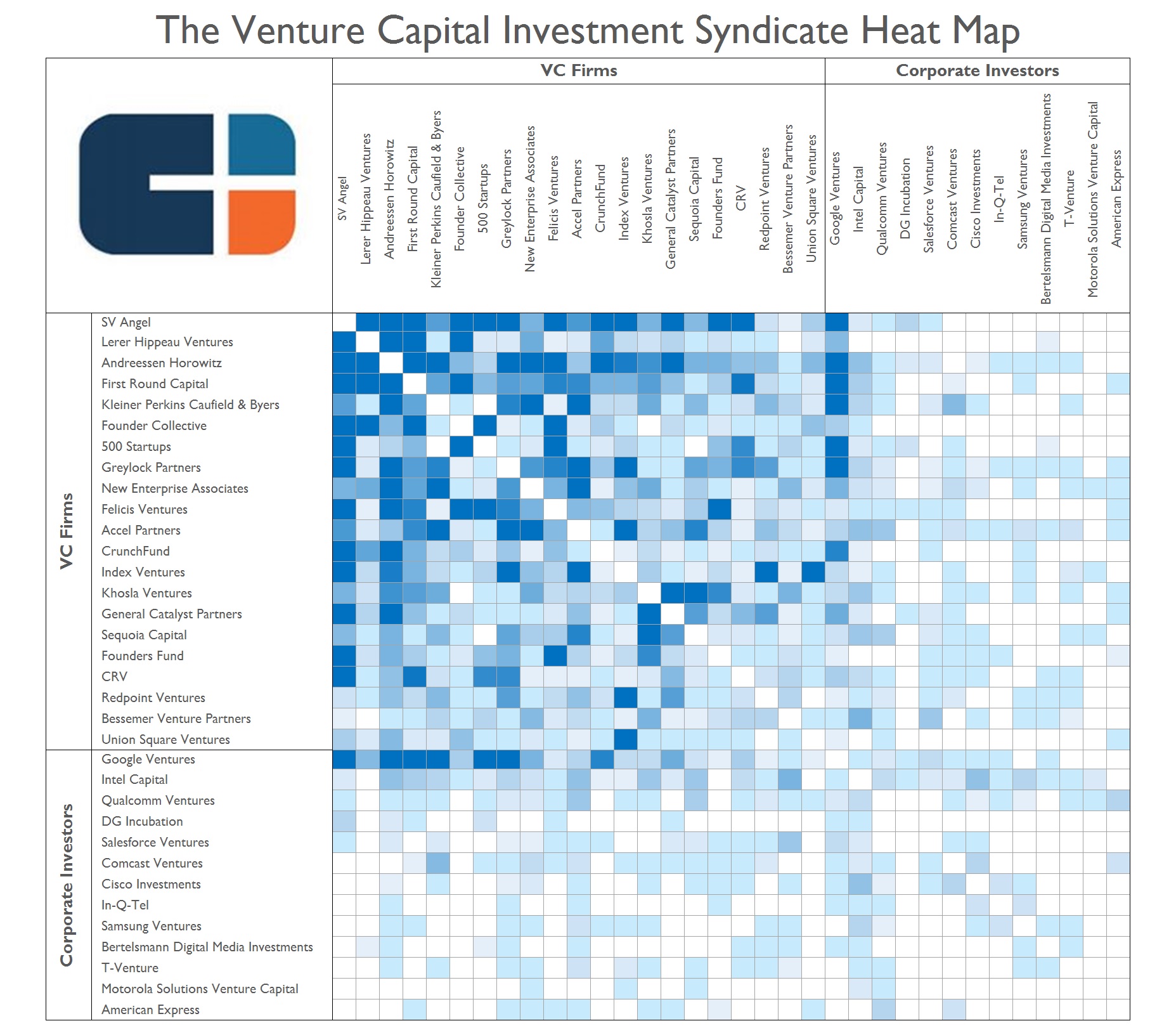

VC relationships are represented as a matrix. The portfolios can be read from top to bottom or left to right. The red hot spots represent high growth investments. VC's in axis x can only invest jointly with VC in axis y. The trigger - as previously stated - is a successful partnership (Think: Red Hot Spot)

It assumes if two VC's have partnered on a successful investment(>5x) they will invite each other to participate in other >5x investments within their collective portfolios.

By doing this the Portfolio Managers are leveraging the latent network effects in the marketplace.