Published Winter 2020

“I'd rather have lucky generals than good ones.”

- Napoleon Bonaparte

The AI powered RoboVC we started building in 2017 has now processed the investments styles of 2000+ VCs and Start-up investors

So what can the accumulated wisdom of the profession teach us about investing in innovation?

The simple answer is not much

But let’s not stop there

The deeper insight is to be found in the WHY?

At a fundamental level you need to understand that VC’s are not very good at innovation portfolio management

Not only are their investments locked up for an extended period (i.e. illiquid)

History shows us few actually manage to 'hit the ball out of the park'

The majority of funds fail to beat the market index

A large percentage lose money

The question being WHY?

Evidence suggests the average VC has has a weak comprehension of portfolio mathematics (e.g. Power Laws, Diversification, Syndication and the Time Value of Money)

For Example

VC’s are quick to explain they only need 1 or 2 investments to deliver =>10x ROI to return the fund

But few comprehend the probability of unearthing => 10x startup investments

Many appear confused by the suggestion the distribution of VC portfolio returns mirror the startups they invest in

Or, that VC’s who consistently out perform the NASDAQ Index are the exception. Not the rule

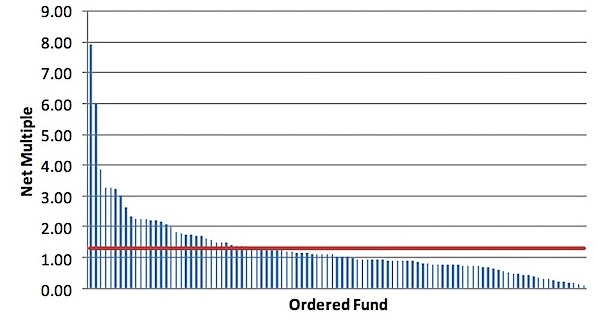

The probability of a VC Fund portfolio delivering +5x is less than 2%

The probability of them repeating that feat is ~0

A Power Curve is just that. There are a handful of outsized winners at the head of the tail. The rest are losers.

This is why, even though the number of exits can be mapped to a bell curve, the averages are meaningless

Likewise those who focus exclusively on investing in seed, early, growth or late stage fail to grasp the mathematical reality of the Time Value of Money…

no stage offers an advantage over any other

and this begs the question:

Would asking VCs to head back to the classroom to learn statistics and probability or spending a weekend in Vegas at the roulette table improve their chances of picking a winner?

Probably not… WHY?

Experiments happen on the edges. Innovation happens on the edges

Progress happens when these experiments mature and become mainstream ways of thinking and doing

When the edge moves to the centre

The role of the VC is to profit from bank rolling this movement from the edge to centre

For this to happen the VC must live on the edge

They must be where the experiments are happening

Truth is most VCs sit in the centre hoping the edge will come to them

Sadly it doesn’t… and, even if it does, they lack the situational awareness to comprehend the opportunity

WHY?

In truth venture capital operates along the lines of the A&R Managers of the 1970's music scene

The lazy sit at home watching the talent shows on TV (Think: Incubators) or listening to the radio (Think: Twitter)

The winners, profiting from the latest disco fade, party the night away at the Studio 54

Outside is a line of wannabes, stretching around the block, trying to get in

Meanwhile a precious few are living life on the edge

Taking in the raw, rough vibe at CBGB. Busy signing up the bands of the New Wave

You see, when it comes to unearthing the next generation of =>10x founders, most VC’s are simply moving in the wrong circles

They suffer from network blindness

The same thing happens every day in large organisations

and here my friends is the lesson the accumulated wisdom of the venture capital industry offers to us

Innovation happens on the edge

If you want to profit from it you need to be there

Searching for that edge

On the edge